Money worries are changing the way Americans shop in 2025. According to a recent Household Sentiment Survey, over half of U.S. households are now watching their budgets more closely. About 70% are also spending less on things they don’t need, like dining out or buying the latest gadgets. With prices staying high and headlines full of news about inflation and tariffs, many families are pushing big purchases down the road and picking less expensive brands when they do shop. Here’s how these trends may affect you—and what you can do to keep your finances steady.

Why Are Americans Putting Off Big Purchases?

Long gone are the days when buying a new TV or booking a spontaneous vacation felt like no big deal. Today, most households are more cautious with their spending, especially on big-ticket items. According to the Household Sentiment Survey reported by HousingWire, only about one-third of families feel hopeful about the economy in the coming year. That means uncertainty—and people tend to hit pause on big spending during times like these.

“When people aren’t sure about the future, they naturally put off big decisions—like buying a car or new furniture—so they have money saved just in case they need it,” says John Burns, a housing industry analyst.

Inflation is a big part of the picture. Many goods—from groceries to clothing—have stayed pricey. Toss in worries about new tariffs (which can make imports cost more), and it’s no wonder that budgets are feeling tight. Some shoppers are also dealing with bigger bills for credit cards, rent, or utilities, which means there’s less money left over for fun purchases.

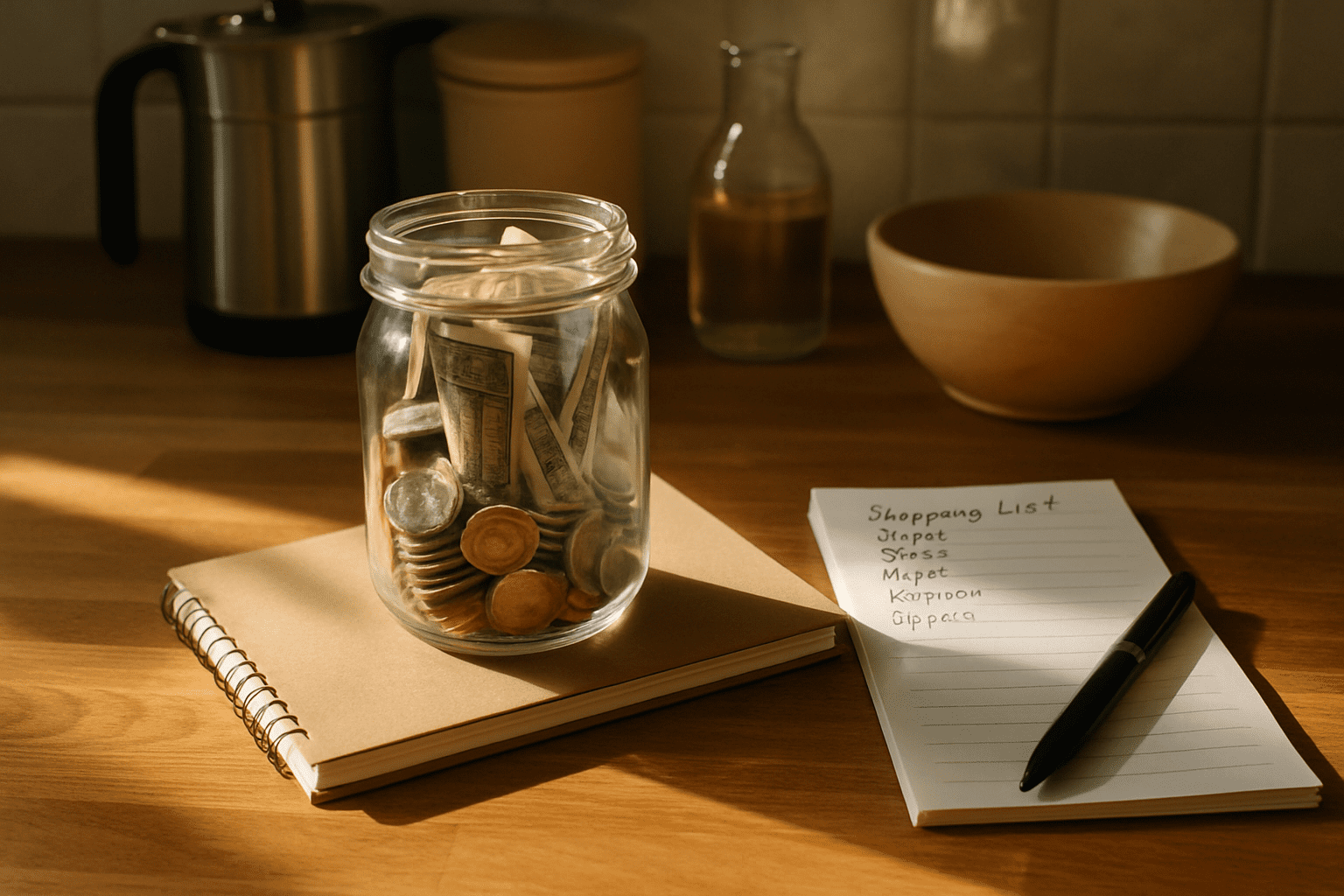

There’s an upside, though. When you put off a big spend, you get extra time to save, shop deals, and reconsider if you really want or need an item. For example, if you were planning to get a new appliance, waiting a few months might land you a sale or let you compare brands for better value.

Here’s what you can do if you’re considering a big purchase:

- Set a clear savings goal and use automatic transfers if possible.

- Check historical price trends—some major purchases go on sale at predictable times of year.

- Look closely at your current needs: could a repair or used item hold you over until the market improves?

By planning ahead and shopping smartly, you may be able to get more for your money, even in a tough economy.

Swapping Brands: How Flexibility Stretches Your Budget

High prices are leading many shoppers to rethink their go-to brands. According to the survey, 70% of Americans are cutting back on “discretionary spending”—that’s everything outside of essentials, like upgrades, name-brand items, and splurges.

“Brand loyalty takes a backseat when families need to tighten their belts. Sometimes the store brand really is just as good—especially for basics like snacks, cleaning supplies, or paper goods,” explains a financial educator at DollarSense.

This shift doesn’t just save you money at checkout. When you’re open to new or store brands, you’ll often find regular sales, coupons, or loyalty perks you might otherwise miss. Consumer Reports often shows that many less expensive brands score just as high as big names, especially for items like cereal, batteries, and even some electronics. For many households, this small change—brand swapping—acts like a silent raise, freeing up dollars that can go toward savings or rising bills.

Here’s how to make the most of brand flexibility:

- Try the generic or store brand for one new product each shopping trip.

- Check online reviews for budget brands before switching—sometimes savings don’t mean less quality.

- Sign up for store loyalty programs; many offer extra discounts on their own products.

- Shop at different stores to see who has the best deals for your new favorites.

Most importantly, keep a running list of products where you don’t notice a difference. You might be surprised by just how many staples you can swap out without feeling the pinch.

Staying Confident and Building a Smarter Plan

Worrying about money is stressful, but it doesn’t have to take over your life. Even with lower consumer confidence—just 34% of families now feel positive about the economy, reports John Burns Research & Consulting—you can still make choices that leave you better off next month, and next year.

“Control what you can, and focus your energy where it counts: on daily habits, building savings, and finding small wins you can celebrate,” says the DollarSense team.

There are several ways to chart a steady course even as prices and uncertainty rise. First, create or revisit your budget. Think of a budget like a roadmap for your paycheck—it shows you exactly where your money goes. With inflation impacting everyday costs, it’s more important than ever to track your expenses and trim where possible.

Next, set micro-goals for your money, like building an emergency fund or paying down one credit card. It’s okay to start small—every extra $10 adds up. Use budgeting apps or simple pen-and-paper methods if high-tech tools feel overwhelming. The goal isn’t perfection, but progress and peace of mind.

Finally, look for positive changes and celebrate small steps. Did you save $20 this week by swapping brands or skipping takeout? Write it down! Remind yourself that these choices are building blocks for a less stressful future.

- Review your spending weekly and highlight one win.

- Talk to a friend or family member about money goals—sometimes just sharing your plan makes it easier to stick to.

- Don’t be afraid to ask for help. Many community centers and libraries offer free classes on budgeting or saving.

Taking small steps, adjusting your spending, and staying open to new habits can turn economic uncertainty into an opportunity to build resilience. It won’t happen overnight, but with patience and flexibility, your money worries can take a backseat—even in challenging times.