Broke Folks Swear By These 6 Sneaky Money Moves—The Rich Are Clueless

You keep hearing the same tired advice: skip lattes, coupon hard, pray for a raise. Yawn. Meanwhile, people living paycheck-to-paycheck are pulling off mind-blowing money maneuvers Wall Street bros never see coming. Ready to rip a few pages from their survival playbook before prices jump again this year? Strap in—your wallet is about to feel lighter in the best possible way.

The Underground Lending Circle That Turns Pennies Into Lifelines

Pretend your bank ghosted you tomorrow. No credit score love, no overdraft wiggle room—nothing. That’s daily reality for millions scraping by. So they built their own bank: rotating lending circles, sometimes called a rosca or susu. Friends, neighbors, even WhatsApp buddies toss cash into one pot; each week someone different takes the haul. Nobody pays interest, nobody waits on hold, and late fees? Zero.

This is the secret handshake lending circle rich folks scoff at but can’t match for speed. You tap money fast for school supplies, rent gaps, or clutch bulk buys—then repay when your turn comes. Trust replaces paperwork, and peer pressure keeps deadbeats out.

“Low-income households are more likely to engage in community-based financial support systems, such as informal lending circles, to manage expenses” (Financial Studies Journal).

- Hack #1: Start tiny—five friends, five bucks a week. No stress, instant discipline.

- Hack #2: Choose a killer name (Money Mob, Savers Syndicate) to cement loyalty.

- Hack #3: Vote a treasurer. Rotate each month so nobody feels bossed around.

- Hack #4: Keep receipts in a group chat pic thread—transparency kills drama.

Here’s how to use this: Set your payday reminder right now; when you see your share stacking, funnel part into a high-yield savings account for double gains. Next up, you’ll discover how broke shoppers beat grocery-store inflation without coupon clipping.

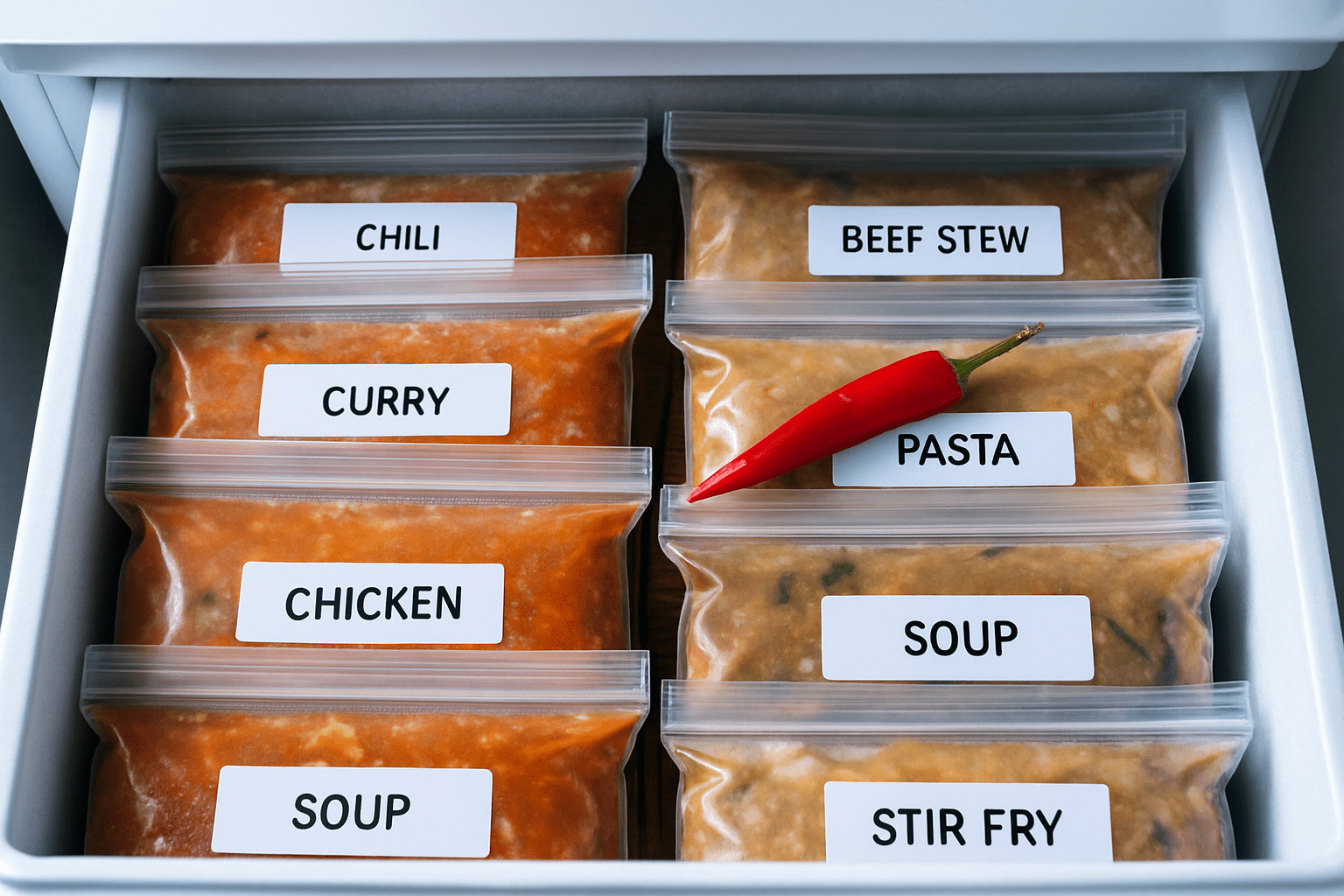

Meal-Plan Street Smarts: Outsmart the Grocery Cart Trap

You know that budget buster called “What’s for dinner?” Low-income families solved it ages ago: they weaponize the freezer and hijack unit pricing. The strategy starts with one ruthlessly planned shopping trip, no fancy apps required. Picture a cart piled high with plain-label rice, frozen veg, and protein bargains snagged at the meat counter’s last-hour markdown.

Call it the two-week pantry reset secret—a full fridge today that slashes impulse buys tomorrow. Instead of nightly drive-thru panic, dinner is pre-batched, seasoned, and chilling, waiting for reheating greatness.

“Individuals with lower incomes often develop creative budgeting strategies, like meal planning and bulk purchasing, to stretch their resources further” (Economic Research Review).

- Batch cook once, eat thrice. Chili, stir-fry, then taco night from the same base.

- Freeze in flat bags—faster thawing, zero wasted shelf space.

- Break packages down to single-serve portions so nothing molds in the back.

- Use the “$1 per pound” rule: if it costs more, wait for a sale or substitute.

- Store grocery cash in an envelope labeled FIGHT INFLATION—psychology wins.

Here’s how to use this: Add up last month’s random snack runs; redirect half that cash toward a warehouse-club day pass. You’ll feel the savings immediately at checkout. Stick around—after the break, we’re exposing the delayed-gratification glitch rich people keep ignoring.

Delay-or-Die Purchases: The 48-Hour Rule Poor Families Live By

Swipe now, cry later—that’s the rich-kid vibe when every shiny gadget drops. Folks who can’t afford regret have a smarter line of defense: delay every non-essential buy by 48 hours. Sounds too simple? It’s the mental speed bump that murders impulse shopping dead.

This 48-hour wallet lock starts as a survival tactic and morphs into an investing engine. Skip the want today, stash the cash tomorrow, and suddenly compound interest is your BFF.

“People facing financial hardship are more likely to prioritize essential expenses and delay non-essential purchases, demonstrating a focus on immediate needs” (Consumer Behavior Insights).

- Step 1: Screenshot the item, then delete the store app. Out of sight, saved money.

- Step 2: Park the would-be spend in a micro-investing account like Acorns or Public. Watch pennies turn into shares.

- Step 3: If you still crave it after 48 hours, hunt for a used version or swap group.

- Step 4: Celebrate each “no-buy” victory—transfer $5 to a dream goal jar as a dopamine hit.

Here’s how to use this: Next time your thumb hovers over Buy Now, set a phone timer for 2 days. When it dings, check your brokerage balance instead of your doorstep. The tiny choices broke folks mastered could stack six-figure wealth over time.